Let me start by saying I get it. While I am not mechanically inclined, I appreciate a well-appointed ride with some power and handling. And don’t get me started on that new car smell. But I’ve learned over the years through car buying mistakes (my own and others) that over-extending on a car purchase is an easy way to put your budget on its ear and derail other financial priorities. Let’s look at some guidelines you can follow to make sure you don’t bust the budget when buying that next car.

Start With Your Gross Income

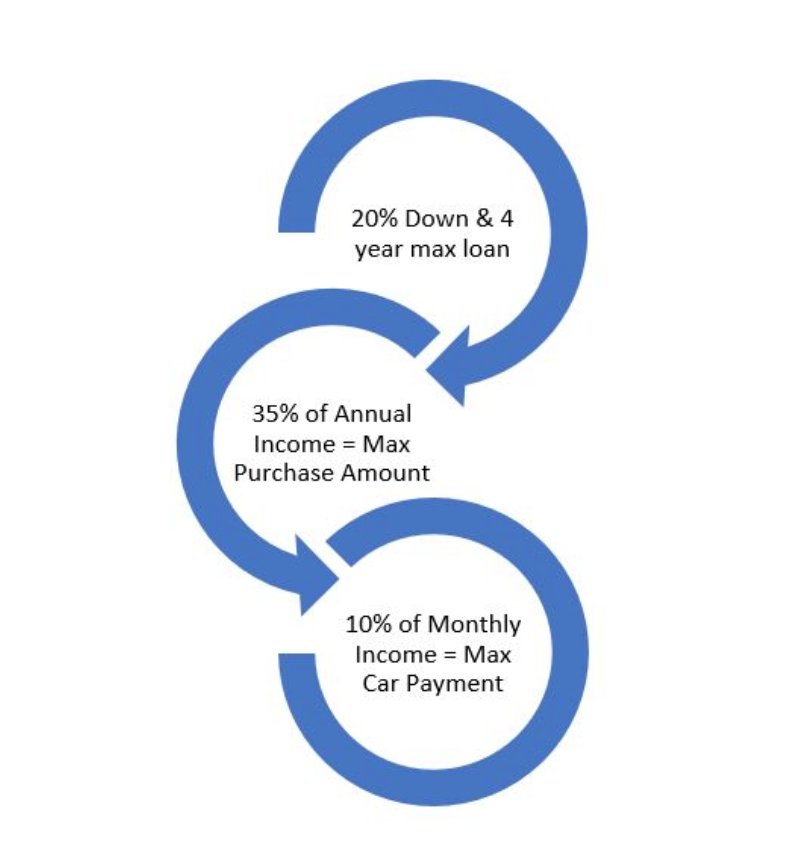

To get an idea of how much car you can afford, a good rule of thumb is to pay no more than 35% of your annual pre-tax income. So, if you make $50,000 before taxes per year, your car purchase price should not exceed $17,500. But you can’t buy a new car for $17,500, you may be thinking. You’re right, but you can find a good used car for that amount (more on that later).

The 20/4/10 Ratio for Car Financing

If you plan to finance your car purchase, follow the 20/4/10 rule: 20% down, loan no longer than 4 years, and keep total car payment – including insurance – to a maximum of 10% of your gross monthly income. This will help you to keep your payments and interest costs down while not losing sight of your other financial goals.

{kind=link}

- Put at least 20% down: This will help lower your monthly payments, but it also protects you from the dramatic loss in value new cars experience (another great reason to buy used). A new car can lose up to 19% of its value in the first year alone. If you put less than 20% down, you can owe more than the car is worth almost right away. This can be an issue if you need to sell before the car is paid off or if the car gets totaled in an accident.

- Term of the loan no more than 4 years: The longer you make car payments, the more interest you pay. Also, if you are making payments, you must meet the requirements for insurance your lender has, which often means paying higher rates. If you can pay off the car in three years, even better! If you must stretch the loan to five years or longer in order to afford the payments, that may be a sign you are buying too much car.

- Keep total car payment (including interest, principal and insurance) to no more than 10% of your pre-tax income: This will help keep the rest of your budget intact. Having your dream car isn’t worth neglecting your emergency fund, retirement, vacation, or other financial goals. This will also help should your circumstances change, like if you lose your job.

Keep in mind this is just a guideline and everyone’s situation is different. Using a car affordability calculator can help you run your numbers and make a wise decision about your vehicle purchase.

Last Thoughts

As you determine how much car you can afford, keep in mind the costs of fuel and maintenance as part of your process. As we touched on, buying used may provide more value and lessen the hit of depreciation compared to new car. Also, make sure you track your credit prior to applying for a car loan to make sure you can get a low rate with lower payments.

Following these guidelines will help you “stay in your lane” when purchasing your next vehicle!